The International Monetary Fund (IMF) estimates that the pandemic has caused a sudden and deep economic recession. How will it impact the economy in the future? Scientific Director of the Institute of Economic Forecasting of the Russian Academy of Sciences (RAS), Academician Boris Nikolayevich Porfiryev speaks about forecasts and potential consequences.

Boris Nikolayevich Porfiryev is the Scientific Director the Institute of Economic Forecasting of the Russian Academy of Sciences and RAS Academician.

– Our vocabulary has been replenished with the new term “coronavirus” with the emergence of the coronavirus. Which areas of our life has it affected most of all?

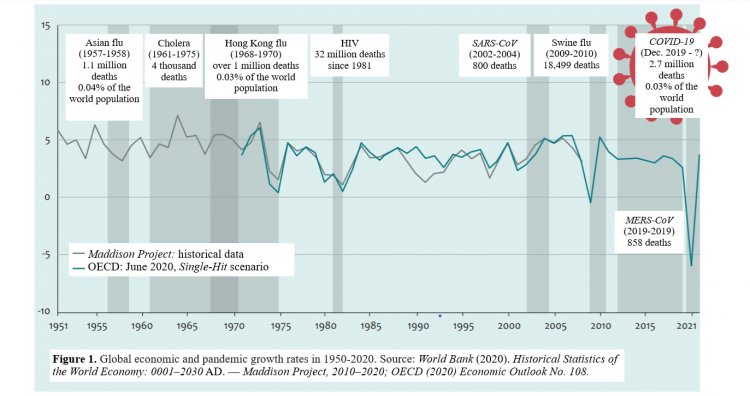

– Indeed, we are used to talk about the coronavirus in the context of medicine and healthcare. The term "coronacrisis" reflects the impact of the pandemic on the entire system of socioeconomic relations that encountered the crisis. This crisis is unique: first of all, it has overtaken all economic systems of the world without exception, although to varying degrees; secondly, it has non-economic causes that are conditional to the coronavirus pandemic and associated restrictions. It is not the first pandemic in the history of mankind; however, it has reportedly led to an economic crisis for the first time in the post-war years. The global economy fell by more than 5% by June 2020 (Fig. 1), and the annual reduction in 2020 was 3.5%. A decline in Russia’s gross domestic product (GDP) was more modest: Rosstat reports that it reduced by 3.1%.

The key cause of this economic recession is the reduction in economic activity due to the strict restrictive anti-epidemic measures introduced by the government. These measures primarily affected the service sector providing the major contribution to the GDP both in developed countries and in Russia. Russia’s service sector is characterized by the highest employment rate and most intense interaction between people. For this reason, the sector experienced the greatest shock from these restrictive measures. Initially, they covered the tourism sector, including air travels. The goal was to minimize infected people’s movement and contacts. As a result, the decline in international tourism reached 74%; air transportation — 60%; in global trade — 15%. Further restrictions were extended to the hotel and restaurant industry.

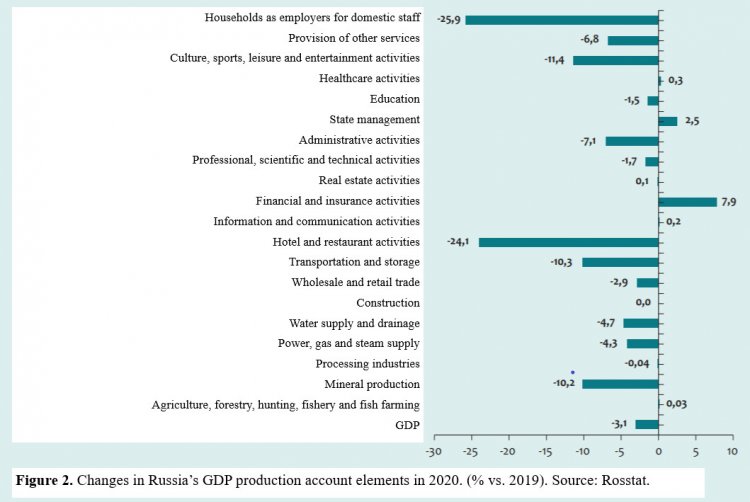

In Russia, the production of added value in these areas decreased by almost a quarter (24%) in 2020, in culture and sports — by more than 11%, in domestic trade — by 3%.

As for manufacture, the decline in the global manufacturing industry was less significant as compared to the service sector (8%), mainly thanks to China; in developed countries, the decline in output in this industry reached 16-17%. Russia managed to maintain this indicator — it reduced by less than 0.1% with significant differences between specific industries and production sectors, while the decline in the mining industry exceeded 10%.

If we look at the consequences of the coronacrisis for the key economic entities, medium and especially small enterprises, including the self-employed individuals, have suffered most of all. In the System of National Accounts, it is reflected in the “Activities of households as employers” section. In Russia, this indicator fell by 26% in 2020, and it is still far from recovery. It immediately affected household consumption in the most negative way. The global indicator declined by over 70% for the first time in the post-war period causing a drop in the global GDP and becoming a unique feature of the current coronacrisis. Russia’s household consumption fell by 4.8% hurting not only the economic performance of this economic sector but also the income of its entities and the entire population of the country. It fell by 3.5% exacerbating the negative downward trend of the previous years.

– Are there any areas where the coronacrisis has brought new growth opportunities?

– Despite the coronacrisis, financial and insurance services increased by almost 8% in the non-production sector in 2020, and public administration costs increased by 2.5%. Government consumption increased by 4% primarily due to the creation and implementation of the anti-crisis support package for the population and national economy, including an increase in budget expenses by more than a quarter. It became the only positive GDP use element. The calculations performed by my colleague, RAS Corresponding Member A. A. Shirov, show that its contribution to economic performance amounted to 0.7%. As I have already been mentioned, the decline slowed down and stopped at minus 3.1% thanks to this factor.

As for the production sector both in the world and in Russia, the introduced anti-epidemic restrictions stimulated an increase in demand for pharmaceutical products, medical services and products, digital products and services that were used more and more actively by the population (significant part of which switched to remote work) and healthcare professionals (telemedicine). It created favorable opportunities for the development of relevant economic activities. In addition, it is worth noting the food and chemical industries as well as agriculture, construction and defense industry enterprises that generally maintained their production rates and, which is important, employment levels primarily thanks to the selective government policy in the application of strict restrictive measures.

– What was the level of state support?

– Various estimates show that the Government of Russia has allocated 4-5% of the GDP to counter the coronacrisis. It is significantly less than, for example, the 2009 anti-crisis program that cost about 10% of the GDP; or other countries’ so-called anti-crisis packages meant for combatting the current coronavirus pandemic and its consequences. For instance, in China, these measures are estimated at 13% of the GDP, in the USA — at 25-26% of the GDP, in Germany, Italy, and Japan — at up to 60%. If we correlate these expenses with the 2020 GDP contraction that was significantly higher in almost all these countries, except China, vs. Russia’s indicator, Russia’s anti-crisis program could be considered relatively effective from a purely macroeconomic point of view.

However, these data do not allow making a conclusion about its integral socioeconomic efficiency: if we take into account the evolution and scale of morbidity and mortality that reached peak values in November 2021, these factors should definitely have negative consequences for human performance and workforce productivity and, consequently, for economic growth and competitiveness. It is no coincidence that forecasts for the next year are less optimistic as opposed to the current year of economic recovery with expected GDP growth rates of 4.3-4.5%. As for the global economy, world business survey findings show that 60% of the respondents consider the pandemic as a threat to future global economic growth; almost half of the respondents — as a threat to national economic growth.

– Why can these measures be not effective enough?

– I’m not a sociologist, so I cannot competently discuss the social behavior of various Russian communities, although it is obviously the most important factor. If we look at the economy, it is worth recalling the beginning of the anti-crisis program when top-priority fields for state support were set, i.e., the most vulnerable population groups were identified, the list of affected industries and economic activities was formed, and the government used this list to allocate grants and subsidies, relax lending conditions, including mortgages, etc. A set of measures providing assistance to households with children and pensioners has been and remains extremely important: the experts from our institute believe that these measures ensured 1.2% of GDP growth and slowed down its overall decrease rate in this way.

Meanwhile, as I have already said, support measures provided to medium and especially small business entities as well as self-employed individuals turned out to be clearly insufficient. Specifically this segment was characterized by the highest drop in income. Despite the increase in wages and pensions, it ultimately led to an overall decline in real personal monetary income and eventually pulled down the entire economy. In my opinion, it is necessary to draw conclusions from this situation, including with regard to the measures to counter the current fourth wave of the pandemic. During this wave, the state had to introduce a non-working week in late October — early November once again.

– The estimates published in the Quarterly Economic Outlook report of the RAS Institute of Economic Forecasting show that the post-crisis recovery of the Russian economy was completed by the end of the first half of the year, and the pre-crisis GDP level was achieved in this April. What measures made it possible? What does it mean for the nation?

– In my opinion, it was achieved thanks to the previously discussed support measures implemented in 2020. In addition, decreasing morbidity had an effect at certain stages, which almost immediately influenced the population’s economic activity. At the same time, as I have already mentioned, Russia did not introduce total business closure as opposed to other countries. A selective approach was used; if quarantine was enforced, it lasted for no more than four to five weeks, which helped the economy recover faster. If a tight quarantine model was used for a longer period, the picture would be different: the experts from our institute believe that the point of unacceptable damage would come in two and a half months of a tight lockdown, and this damage would exceed the volume of the anti-crisis government support package.

Of course, a very significant role was played by pent-up consumer demand. In late 2020 — early 2021, this indicator increased very rapidly, and not all economic entities were ready for this situation, as they hoped for a smoother way out of the crisis. There was a shortage of certain goods, which had an impact on inflationary effects. This rapidly growing demand has become a powerful driver of Russia’s economic recovery, which is expected to reach 4.3-4.5% by the end of this year. Speaking about the growth factors, it is necessary to emphasize that almost half of the contribution to this process comes from consumer demand. Therefore, state support for this indicator is not only a social and humanitarian imperative but also an important economic function. At the same time, it is especially important to support low-income households, households with children and pensioners who primarily consume domestic products, which is important to the development of import substitution and support of domestic producers, including small and medium businesses.

– Every state should have some kind of plan to cope with unforeseen situations and crises. To what extent were the world and Russia in particular ready or not ready for the pandemic?

– Of course, such plans are being prepared by relevant structures both in the world and in Russia. I know this aspect very well, since I have been looking into the matters of economic management in emergency situations for many years. Russia has the Unified State System for Prevention and Elimination of Emergency Situations (RSChS) that involves planning, preparedness and actions, including response to biological and social emergencies, and epidemics belong to this group specifically. As for epidemics, the key coordinators are Russia’s Ministry of Health and Rospotrebnadzor headed by the Chief Public Health Physician. These structures’ planning and actions minimize the risks of such emergencies, and we have been actually observing this effect for many years.

As for the current coronavirus pandemic, the situation is controversial. On the one hand, at the fundamental level, none of the world countries managed to supply a truly effective response to such a large-scale pandemic with, which is especially important, constantly changing (due to mutations) threat factors, except, perhaps, China. Otherwise, where did more than 250 million disease cases and five million deaths come from in the world, including the global economic leader, the United States? In my opinion, the problem is not only the uniqueness of the cause of the pandemic but also certain underestimation of this danger by the states. For instance, until recently, the United States performed only two million tests a day instead of the required 20 million tests per day, that is, 10% of the needed quantity, while $6 million required to perform these tests was 200 times (!) lower than the lockdown costs. Data from Harvard University show that it costs $12 billion a day.

Underestimating the danger of the pandemic has long been typical of the world community as a whole. For example, since 2010, the World Economic Forum held annually in Davos with the participation of leading politicians and businesspeople has been regularly publishing the group's forecasts on global risks for the upcoming decade. All the reports up to 2020 (published in February of 2020) put pandemic risks somewhere in the second tier and well behind the risks of climate changes and natural disasters. Only the 2021 forecast puts pandemic risks in the group of the foremost threats to the economy and society. However, even in this case, after being equated to the risks of climate changes and natural disasters in terms of the scale of expected damage and losses, they were inferior to these risks in the likelihood of such an event. Another example: In connection with the 2003 outbreak (severe acute respiratory syndrome, SARS) and 2012 outbreak (middle east respiratory syndrome, MERS), the World Health Organization (WHO) has repeatedly raised the issue of growing coronavirus pandemic threat and need to include this risk into the list of top priorities for national systems for emergency preparedness and response planning systems and intergovernmental cooperation in this area. However, this call from the WHO was not properly heard and perceived, which, of course, affected the effectiveness of planning.

On the other hand, speaking about our country, the domestic RSChS system responded well at the first stage when the threat suddenly arose, and no one could assess its true scale and severity primarily due to the fact that this virus was previously unknown to medical science. Preceding experience in epidemiology, including Ebola vaccine developments, made it possible to create several coronavirus vaccines at once in the shortest possible time. In addition, healthcare professionals’ skillful and selfless actions helped significantly alleviate the situation. It is worth noting that the RSChS system played an integral role coordinating healthcare professionals’ activities with Russia’s Ministry of Defense that helped quickly build hospitals and allocated military physicians there. It is essential to recall the above mentioned anti-crisis program of the government. Are all these aspects connected with planning and readiness? Does it testify to their effectiveness? In my opinion, it is certain.

At the same time, the current pandemic has clearly confirmed the urgent need for qualitative improvement in Russia’s healthcare system (and not only in this system). The domestic healthcare system was once based on the preventive medicine principles and priorities described and implemented by N.A. Semashko (Soviet party and state official, one of the creators of the Soviet healthcare system — editor’s note). They produced remarkable results, and many foreign colleagues used to consider the Soviet healthcare system to be exemplary thanks to this fact. Unfortunately, many things were lost in the 1990s, and further development was not smooth at all. However, we still have a foundation to create and develop an up-to-date healthcare system by reinforcing not only material and technical resources but also human and financial resources. In the latter case, it seems rational to look once again at the corresponding budget item for 2022 and 2023-2024. Now this budget item suggests a small reduction in constant prices for healthcare expenses.

There is another organizational consideration related to the lessons drawn from the current pandemic, more specifically, to a voluntary vaccination approach. Let's not question the democratic principles, but the effectiveness of this vaccination approach in different countries is questionable. The fourth wave of the pandemic is practically entirely connected with many people’s unwillingness to undergo vaccination, which creates risks for the society as a whole and, in fact, devalues the choice made by an equally significant share of people who received vaccination. However, it contradicts the democratic principles. Obviously, more balanced solutions are needed to take into account such disagreements. In any case, they should not endanger the safety of the public. Therefore, now many states make decisions on compulsory vaccination for specific population categories, first of all, public employees, healthcare professionals, service and public catering workers. It seems that such a model of action should have been implemented much earlier, including in Russia.

– Are there any forecasts of what the post-pandemic world will be like and when we will be able to step over this situation?

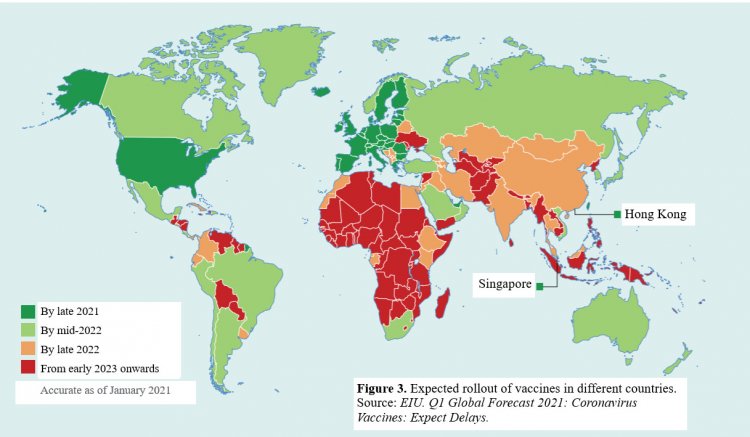

– Forecasts are always available. In my opinion, it is too early to say that the post-pandemic world is almost at the door. Nevertheless, discussions about “bright future” intensified in late 2020 when morbidity and mortality rates decreased in many countries of the world causing a certain surge of optimism. However, now it is clear that optimism has not been justified yet primarily due to the low vaccination rates, especially in developing countries. The forecast made by British analysts from the Economic Intelligence Unit, a subdivision of the authoritative The Economist weekly newspaper, in January 2021, shows that the situation with vaccines will not stabilize until late 2022. By the fall of 2021, the situation seemed to be significantly better than this forecast in several developed countries and China that achieved the vaccination rate of almost 70%. However, the prospects for the least developed countries remain, to put it lightly, bleak at least until late 2022 — early 2023 (Figure 3). It will hardly be possible, as you put it, to “step over this situation” until this moment.

If we try to look beyond this horizon, hopefully, the world will learn the harsh lessons of the COVID-19 pandemic, coronacrisis and overlapping consequences of the natural disasters, energy crisis and political conflicts, so it will pay significantly more attention to risk management efficiency. An important role in this process should be played by the digital economy as well as information and communication technologies that will be used more actively: from monitoring systems and emergency alert systems, production and logistics management to remote work, training, disease diagnostics and treatment. As you know, the ICT sector has showed strong growth rates amid the pandemic.

People have switched to remote work and education, which triggered the development of communication technologies; demand for digital medicine services has increased sharply. It refers to not only transferring patient data to the digital format but also the use of telemedicine for consultations and treatment. This trend was observed even before the pandemic. However, specifically the events of 2020 spurred the development of this area.

Speaking about the macroeconomic, strategic point of view, the pandemic has not changed the fundamental challenges faced by Russia’s economy: technological and structural modernization — qualitative improvement in the economic structure, first of all, in favor of processing industries, use of the best available technologies and development of hi-tech industries. At the same time, it is not about abandoning the base material sector: our experience shows that the relative stability of Russia’s economy to such challenges is based on its structure, and the base material sector occupies a significant part of this structure. The economic system with the predominance of raw materials in the export structure and end products in the import structure turned out to be more resilient to the crisis. The same circumstance allowed Russia’s economy to withstand the 2009 crisis.

Now it is customary to criticize the base material sector and call it a “resource curse.” However, everything should be approached very carefully. There is no need for crossing the line and going too far. It does not mean that we need to continue to export raw materials until the end of our days, although it would be extremely wrong not to meet global demand, as it was demonstrated by the examples of missed coal export opportunities in 2020 and use of gas export opportunities in the fall of 2021. It is necessary to more deeply process raw materials expanding production and technology chains and export goods with higher added value to increase revenues.

It is even more important to more efficiently use energy and mineral resources within the country. Russia is significantly inferior to its competitors in the GDP energy intensity indicator primarily mainly due to its technological lag. The best available and most promising technologies are more productive, labor-saving (which is important for Russia given the shortage of labor resources aggravated by the consequences of the pandemic) and environmentally friendly, including in terms of climatic criteria. Only the extensive use of such technologies can make Russia’s economy competitive and ensure sustainable economic growth.

Model calculations show that, without these transformations, the country is hardly able to achieve the GDP growth rate of over 2% in the long term. The national growth rate will be lower than the global indicator, and, consequently, the country will not achieve the level of income necessary to improve the quality of life. It is the main integral national development goal the achievement of which is inseparably associated with such priorities as human health, education and culture in the national socioeconomic development strategies. It should be supported by increasing financial support from the state. For instance, now total healthcare expenses amount to 5.3% of the GDP, while government expenses are about 3.5% of the GDP, which is definitely not enough.

– What are the estimates for the impact of morbidity and mortality on the economy?

– The impact of this factor on the Russian economy should not be underestimated, especially as the rates of morbidity (the share of cases vs. country’s population) and mortality (the share of deaths vs. the total number of cases) caused by COVID-19 in our country exceed the global indicators, respectively, by x times (55% vs. 3.1%) and 2.5 times (4.5% vs. 2.1%). As we know, the mortality rate reached unprecedented values over the entire pandemic in November 2021: more than 1,000 people per day.

According to different estimates, the contribution of mortality to the GDP decline dynamics in 2020 was about 0.2 percentage points (I am unaware of similar estimates for the effect of morbidity on economic growth). As for another dimension, i.e. the socioeconomic burden of the so-called excess mortality and morbidity, we need a different estimate here, and namely – the cost of life and health losses in relation to the GDP. Such an assessment is made using an indicator of the economic value of a human life (statisticians call it the “value of a statistical life” – VSL) to substantiate the required level of expenses to save (protect) this life. The estimates for Russia vary: from 4 million rubles (Rospotrebnadzor) to 20 million rubles (the World Bank). According to my calculations, anyway, based on the scale of excess mortality caused by the direct and indirect impact of COVID-19 in 2020 estimated by Rosstat at 163 thousand people (2021 forecast – 400 thousand), the social burden on the economy equals 1,3% of the GDP (2021 forecast – 3.3-3.5% of the GDP).

As for the economic burden of morbidity, as you might know, almost 8 million out of 9.3 million coronavirus patients recovered in Russia as of November 20, 2021. To be more accurate, they closed their sick leaves, taking into account that Russian doctors (like their colleagues in other countries) register serious health problems in many people who have experienced the disease and some of them are again hospitalized with complications caused by coronavirus consequences. According to WHO estimates, about 10% of the patients experience a severe disease course, which means significant negative consequences for their ability to work, not to mention employees’ performance and creativity. If we focus on this assessment, according to our expert and even conservative estimate, the socioeconomic burden caused by this factor is at least not inferior to that of excess mortality. Thus, the cumulative load on the economy in 2020 reached about 3% of the GDP (which is comparable with its reduction value amounting to 3.5%). It has been estimated that this indicator will double in 2021.

– You have already mentioned the 2008 crisis several times. It seems to me that at that time the entire world came out of it through cooperation and joint activities. Why now, when we know our common enemy, do the states have no wish to join forces?

– The world really came out of the crisis quite quickly in 2009, although the pace and efficiency of this recovery significantly varied from country to country. Some of them are still experiencing serious hardships. At the same time, like now, there was some kind of cooperation of actions, but I cannot call it full interaction. That crisis, unlike the current coronacrisis, had a cyclical nature, and the methods of its settlement were well-known and consequently promptly used. At that time, the most vulnerable sector was financial, so all countries, including Russia, were actively using state support packages where resources to help banks and other financial institutions prevailed, while the assistance to the real sector of the economy was much more modest. According to different estimates, these support measures in Russia cost from 10 to 11% of the GDP.

Now the situation is absolutely different. The coronacrisis was caused by factors other than economic, the negative trends in the economy were primarily due to the restrictive measures that entailed a drop in production, income, etc. In other words, the nature of the crisis turned out to be different and so it primarily required support not for the financial sector but for the real sector of economy and especially households, as well as the most vulnerable groups of the population (which was done by the government, but we have already discussed the efficiency of these measures with you earlier). Besides, it required – and this is the main thing – efforts to suppress the pandemic itself – primarily through vaccination, the need for which, unfortunately, is still underestimated by the population, despite authorities’ efforts and its efficacy. The latter is confirmed not only by domestic experience, but also by world statistics.

At the same time, you are absolutely right when talking about cooperation of states’ efforts to combat the pandemic that, being a global phenomenon, objectively requires strengthening joint actions. However, unfortunately, the world continues to follow the path of regionalization and isolation – roughly speaking, every man for himself. This trend is also clearly seen in geopolicy – just remember all these sanctions that are only getting tougher, even despite the pandemic and people’s suffering, and in the economy, which is confirmed by the example of vaccines. Their developers and manufacturers, i.e. pharmaceutical companies characterized by an exceptionally high degree of monopolization, found themselves at the heart of it all and took full advantage of what was happening.

Let us recall the situation around the domestic vaccine Sputnik V that was rejected in Europe and the United States, Japan and was not even approved by WHO – not because it is ineffective, but rather for opposite reasons: its efficacy turns domestic companies and Russia into a serious competitor being able to cover a significant part of the world market of medicines and medical products. You may also recall the situation with the supply, or rather the shortage, of vaccines made by pharmaceutical giants from the same developed countries to developing countries. It is clear that in a market economy corporations try to take advantage of the existing demand, but during the hard times of human history they should have been guided by social and humanitarian considerations. Besides, today the use of the so-called ESG (environmental, social and governance) criteria as the main indicators of companies’ success ratings are almost the main trend in the development and motto of western businesses. However, they are almost exceptionally applied to the climate challenge and become neglected for some reason when it comes to the coronacrisis and its consequences.

– Today, we have talked a lot about economic indicators and forecasts, including those made at your institute. Please tell me about its history.

– The Institute, as its name suggests, deals with short-, medium- and long-term forecasts of our economic development. Academician V. V. Ivanter, one of the founders of the modern RAS Institute of Economic Forecasting and its director for 20 years, used to say that such a forecast is not a prediction of the future – it is rather an analysis and assessment of the consequences of implementing selected decisions (development scenarios). Forecasts are made using the modeling tools that have been developed and constantly improved by the specialists of our institute over the 35-year period of its existence since 1986. At that time, the laboratory of the Central Economics and Mathematics Institute of the USSR Academy of Sciences was transformed into a new institute through the efforts of Academician A. I. Anchishkin, an authoritative practical economist working for the USSR State Planning Committee and being the founder of the Institute of Economic Forecasting of the Russian Academy of Sciences, to provide serious powerful intellectual support for the academic community dealing with the scientific and technological modernization of the economy direly needed by the country at that time. As you might see, this objective is still relevant.

I. Anchishkin suddenly died, his position was taken by Academician Yu. V. Yaremenko who not only continued implementing his predecessor’s plans, but also gave a new strong impetus to the development of our institute, including the creation of a new research methodology and economic and mathematical models.

– What tools do the employees of your institute use?

– Their arsenal is quite wide, it covers practically the entire range of tools known to economic science. It is based on the input-output balance models that were developed in our country and became famous thanks to one of their creators, V. V. Leontyev, the 1973 Nobel laureate in economics. These models are being constantly improved by my colleagues, true enthusiasts in their profession and world-class specialists, which is annually confirmed by their participation in major international conferences, seminars and joint scientific research studies.

I am very happy that the research and forecasts by the RAS Institute of Economic Forecasting are in demand by both the scientific community and especially the state and corporate governance sector, at the international level, in the healthcare sector, including support for decision-making to counter the coronavirus pandemic, improvement of models used to assess and forecast the consequences of the pandemic in Russia. I am really glad that there are many young scientists among our employees. They are the future of both our science and our country.

The interview was conducted with the support of the Ministry of Science and Higher Education of the Russian Federation and the Russian Academy of Sciences.

{kind=link}